A startup loan is a form of debt financing designed for new businesses. Since new companies don't have years of revenue history, lenders focus on the founder's personal credit, the strength of the business plan, and projected future earnings to provide the capital needed for hiring, marketing, or inventory.

Why Your Startup Needs a Funding Roadmap

You’ve poured everything into a product that solves a real problem. The feedback is great, users are trickling in, and you've nailed your messaging. But you’ve hit a wall. Growth isn’t happening on its own—it needs fuel.

That feeling of being stuck is familiar to almost every founder. You know that scaling requires capital, whether it's to hire that key engineer, launch a paid ad campaign, or just give yourself enough runway to close bigger deals. The world of business financing, however, can feel like a maze of jargon and hidden requirements. It’s easy to feel like you need a finance degree just to understand your options.

This guide is your roadmap. We’re not going to throw dense financial theory at you. Instead, we’ll cut through the noise with practical, actionable advice.

The Good News for Founders

If you're worried about securing funding, you're not alone, but there's a positive trend emerging. Lenders are increasingly willing to bet on new ventures. In 2025, U.S. small business lending roared back with a 7.5% jump in the second quarter, hitting near-record SBA 7(a) approvals.

Better yet, startups under two years old saw a 28% surge in applications and 22% more approvals, proving that lenders are actively funding new businesses. This shift shows a growing confidence in early-stage companies.

This guide will help you understand the different types of loans out there and figure out which one actually fits your situation. We'll cover everything from what lenders look for to how to navigate the application process with confidence. By the end, you'll have a clear framework for making smart funding decisions. For SaaS founders, in particular, understanding these options is crucial for scaling your product effectively. To get a better sense of how this applies, check out our guide on what is a SaaS product.

Choosing the Right Type of Startup Loan

Picking a startup loan can feel like staring at a wall of tools for a job you've never done before. You see names like "term loan," "line of credit," and "SBA loan," and they all sound vaguely the same. The secret isn't to memorize dictionary definitions but to match the financial tool to the specific job you need done right now.

Think of it this way: you wouldn't use a hammer to drive a screw. In the same vein, the loan that’s perfect for buying a big piece of equipment is completely wrong for managing unpredictable monthly expenses. Your goal is to find the funding structure that solves your immediate growth challenge, not just the one with the lowest advertised interest rate.

Matching the Loan to Your Mission

Instead of getting lost in financial jargon, let’s frame the most common startup loans around the problems they actually solve. This approach keeps you focused on your business need first, so you can then find the product that fits.

For Unpredictable Cash Flow: The Business Line of Credit A business line of credit is a lot like a company credit card, just with much better terms. It's a revolving pool of cash you can draw from when you need it, pay back, and draw from again. It’s the perfect solution for smoothing out cash flow gaps, like covering payroll while you wait for a big client invoice to clear.

For a Specific, One-Time Purchase: The Term Loan A term loan is refreshingly straightforward: you get a lump sum of cash upfront and pay it back with interest over a set period. This is your go-to for a single, strategic investment with a clear ROI—think a major server upgrade, an office build-out, or even acquiring a smaller company.

For SaaS Growth: Revenue-Based Financing (RBF) Designed specifically for businesses with predictable, recurring revenue (hello, SaaS companies), RBF gives you an advance on your future sales. Your repayments are a percentage of your monthly revenue, so they scale up or down with your performance. This makes it a super flexible option for funding a big marketing push or sales expansion without giving up any equity.

For Government-Backed Security: The SBA Loan SBA loans are partially guaranteed by the U.S. Small Business Administration, which means the government takes on some of the lender's risk. This translates into favorable terms and lower interest rates for you. The trade-off? A much longer, more document-heavy application process. They're better for well-planned, long-term growth initiatives, not for "I need cash yesterday" moments.

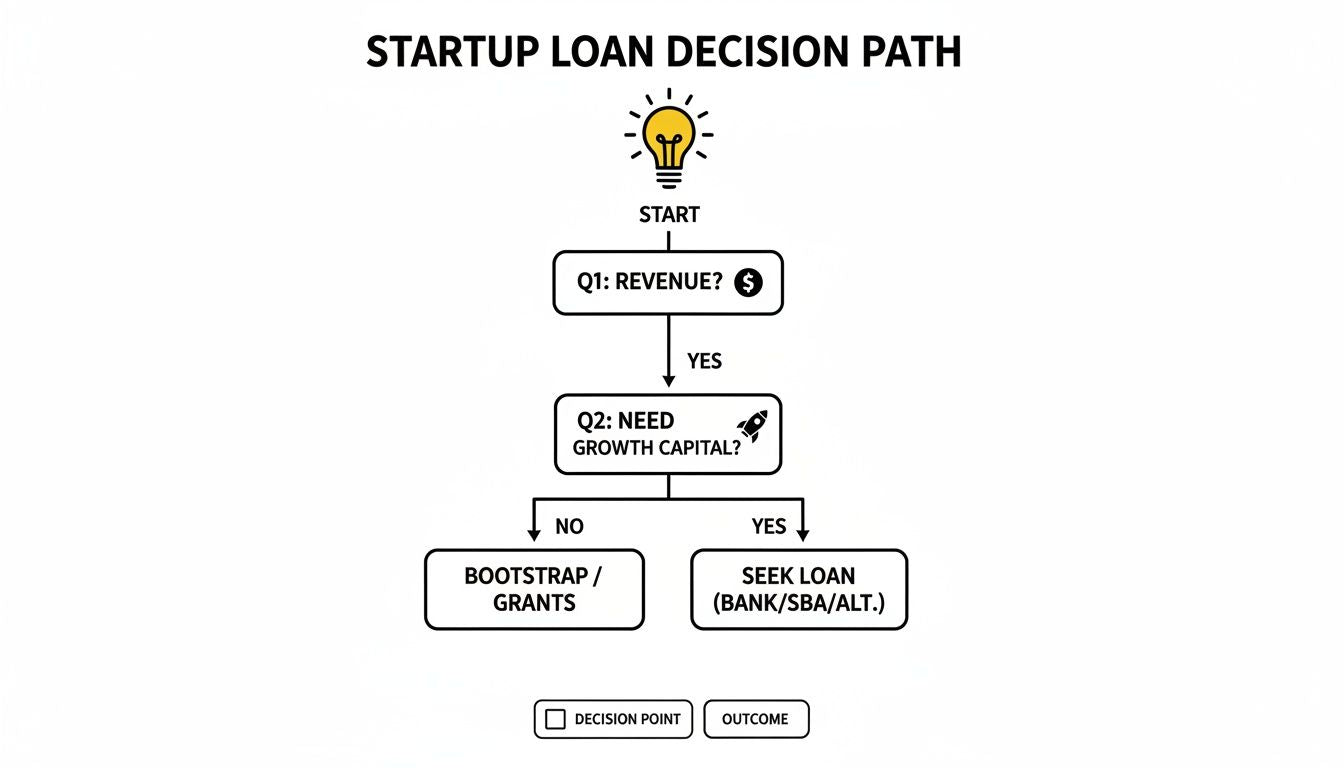

This flowchart can help you visualize the decision path based on where your startup is today and what you're trying to achieve.

As you can see, your current revenue and your need for growth capital are the two biggest factors steering you toward the right kind of financing.

Comparing Startup Loan Types Side-by-Side

Once you’ve figured out the job your loan needs to do, it's time to get into the details. The fine print really matters here, as it directly impacts your costs, your repayment obligations, and ultimately, your control over the company. A loan is much more than a dollar amount; it's a strategic partnership with real financial consequences.

Here's a simple breakdown of how the most common loan types stack up against each other on the factors that matter most to founders.

Loan Type

Typical Amount

Interest Rate Range

Repayment Structure

Impact on Equity

SBA Loan

$50k - $5M

Low (Prime + spread)

Fixed Monthly Payments

None

Term Loan

$25k - $500k

Moderate to High

Fixed Monthly Payments

None

Line of Credit

$10k - $250k

Moderate to High

Pay Interest on Draws

None

RBF

Varies (based on MRR)

High (Factor Rate)

% of Monthly Revenue

None

This table makes it clear that while an option like RBF offers incredible flexibility, it often comes at a higher effective cost. On the flip side, SBA loans have fantastic terms but demand a lot more patience and paperwork during the application process.

The Founder's Dilemma: Convertible Notes

There's one more popular option that blurs the line between debt and equity: the convertible note. It starts its life as a loan but is designed to convert into equity (company stock) during a future funding round.

A convertible note is essentially a bet on your future success. Investors give you cash now, and instead of getting paid back in dollars, they get a piece of your company later—usually at a discount.

It's a common choice for very early-stage startups that are too new to have a clear valuation. While it can be a fast way to get capital from angel investors, it's critical to understand that you're committing to selling a portion of your company down the line.

Ultimately, picking the right startup loan comes down to a clear-eyed assessment of your immediate business needs, your tolerance for risk, and your long-term vision. Each option presents a different trade-off between speed, cost, and control.

What Lenders Actually Want to See from You

Applying for a startup loan unprepared is the business equivalent of showing up to a demo with a half-built product. It doesn't matter how great your idea is; if the presentation is a mess, you've already lost the room. Lenders aren’t just looking at numbers on a page—they’re trying to figure out if you're a good bet.

Walking in with a disorganized pile of documents sends a clear signal: you're not ready. A well-prepared application, on the other hand, tells them you’re a serious founder who sweats the details. It's all about building confidence from that very first interaction.

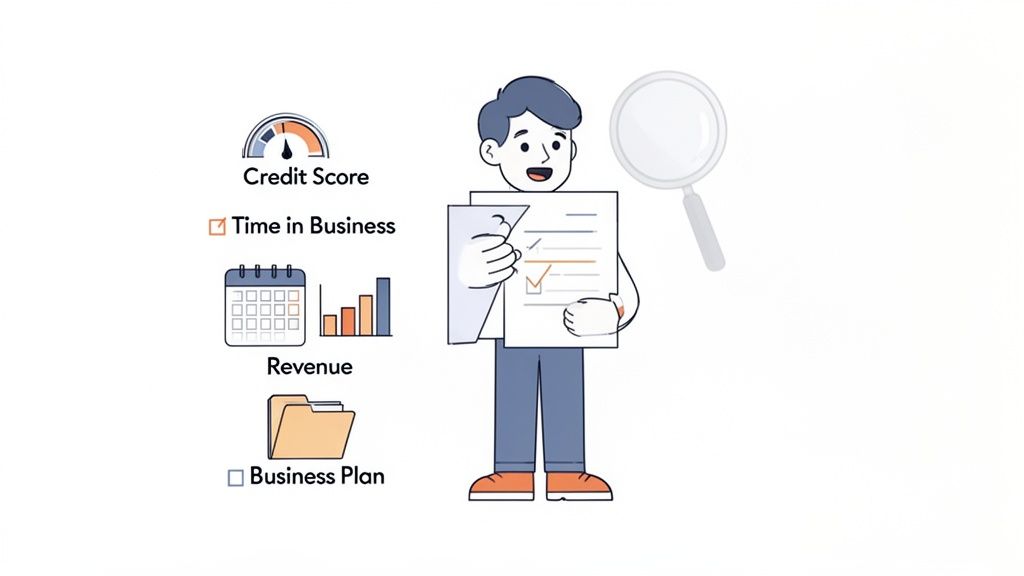

The Non-Negotiable Metrics

Before you even start crafting your company’s story, lenders will glance at a few core metrics to see if you meet their basic criteria. Think of these as the gatekeepers. If you don't pass this initial check, the rest of your application might not even get a serious look.

Your Personal Credit Score: This is a big one. For an early-stage company, lenders often see your personal financial habits as a proxy for your business discipline. A strong score (typically 680 or higher) suggests reliability.

Time in Business: Most traditional banks want to see at least one to two years of operating history. Newer fintech lenders are often more flexible, but having some track record always helps.

Annual Revenue: Lenders need to see a clear path to repayment. Consistent monthly recurring revenue (MRR) or a solid annual revenue stream shows your business has a pulse and can generate the cash needed to cover loan payments.

Your Business Plan Is Your Pitch

Many founders treat the business plan as a chore—a dusty document filled with buzzwords. That's a huge mistake. Your business plan is the story of your company's future. It’s the script for your most important demo, and the lender is your audience. It needs to be compelling, logical, and backed by evidence.

A great business plan doesn't just list features; it communicates a vision and a clear path to get there. It shows you understand your market, your customers, and your finances. In a way, it’s not that different from creating a product video that clearly explains value. If you need inspiration on structuring a narrative, reviewing some of the best SaaS product videos can show you how to tell a powerful story concisely.

Lenders are fundamentally risk managers. Your job isn't to convince them your startup is the next unicorn; it's to convince them you have a credible, well-thought-out plan to repay their loan.

This shift in perspective changes everything. It moves the conversation from speculative hype to grounded strategy.

The Essential Document Checklist

Confidence comes from preparation. Don't wait for a lender to ask for these documents; have them organized and ready to go. This simple act of being prepared can dramatically speed up the application process and make a powerful first impression.

Your loan application package should include:

Financial Statements: At a minimum, this includes your Profit & Loss (P&L) statement, balance sheet, and cash flow statement for the past 1-2 years.

Business Bank Statements: Provide the last 6-12 months of statements to show your company's cash flow in real-time.

Personal and Business Tax Returns: Have the last two years of returns for both yourself and the business on hand.

Legal Documents: This includes your articles of incorporation, business licenses, and any contracts with major clients.

Detailed Use of Funds: A specific breakdown of exactly how you plan to use the loan capital and the expected return on that investment.

Navigating the Startup Loan Application Process

Think of your loan application not as paperwork, but as a performance. It's the story of your company’s future, and in this story, every single detail matters. The whole process can feel like a mountain to climb, but when you break it down into a series of clear, manageable steps, it becomes a strategic project instead of an overwhelming obstacle.

Treat it like a funding campaign where preparation and clarity are your biggest assets. By tackling it methodically, you’ll present yourself as a competent, reliable founder—exactly the kind of person lenders want to back.

Step 1: Assess Your True Needs

Before you even think about lenders, look inward at your business. The single most common mistake founders make is asking for a vague, rounded-up number. You need to know exactly how much capital you need and, more importantly, what you’ll do with every single dollar.

Create a detailed "use of funds" document. Will the money go toward hiring two specific software engineers? Launching a targeted ad campaign with a projected customer acquisition cost? Be precise. This isn't just for the lender; it's a critical strategic exercise for you and your team.

Step 2: Assemble Your Document Arsenal

We went over the essential document checklist earlier. Now’s the time to gather everything into a single, organized digital folder. Having your tax returns, business plan, and financial statements ready to go before you start applying signals that you are serious and prepared.

This prep work does more than just save time. It builds your own confidence and ensures you can fire back a response to any lender request immediately, keeping the momentum going.

Step 3: Research and Shortlist Lenders

Don't just apply to the first lender you find on Google. The world of startup financing is surprisingly diverse, and the right partner can make all the difference. Your research should focus on finding a lender whose specialty aligns with your business stage, industry, and funding needs.

Traditional Banks: Best for established businesses with at least two years of history and strong collateral. They offer great rates but are notoriously slow and risk-averse.

SBA Lenders: These are banks offering government-backed loans. The process is document-heavy, but the terms are excellent if you can get through the paperwork and qualify.

Online/Fintech Lenders: Ideal for newer startups, SaaS companies with strong MRR, or founders needing capital quickly. They’re far more flexible but often come with higher interest rates.

Pro Tip: Before you apply, clean up your digital footprint. Lenders will Google you and your business. Make sure your LinkedIn profile is professional, your company website is polished, and your social media presence reflects the brand you’re building.

Step 4: Submit a Flawless Application

When you fill out the application, treat it with the same care you’d give your investor pitch deck. Typos, incomplete sections, or inconsistent numbers are immediate red flags suggesting a lack of attention to detail. Double-check every single entry before you hit submit.

You should also have a crisp, one-minute verbal pitch ready. Whether you’re on the phone or in person, you need to explain what your business does, who it serves, and why you need the capital, all in about 60 seconds. Just like a great video can make or break a landing page, a clear pitch can make or break your application. For inspiration on crafting compelling narratives, check out these examples of high-converting landing pages with videos.

Step 5: Understand the Underwriting Process

Once submitted, your application enters underwriting. This is the "black box" where the lender's team verifies all your information, analyzes your financial health, and assesses the risk of lending to you. They will run a hard credit check, review your bank statements for cash flow patterns, and scrutinize your business plan.

Be ready for follow-up questions. An underwriter might call to clarify a large expense or ask for an updated sales forecast. Respond quickly and professionally. This part of the process can take anywhere from a few hours for a fintech lender to several weeks for an SBA loan.

Step 6: Secure and Receive Your Funds

If you're approved, you'll receive a loan offer outlining the terms: the amount, interest rate, repayment schedule, and any fees. Read this document carefully. If you agree, you’ll sign the loan agreement, and the lender will transfer the funds to your business bank account.

Congratulations—you've secured your startup company loan. Now the real work begins: putting that capital to work according to your plan and generating the growth that makes it all worthwhile.

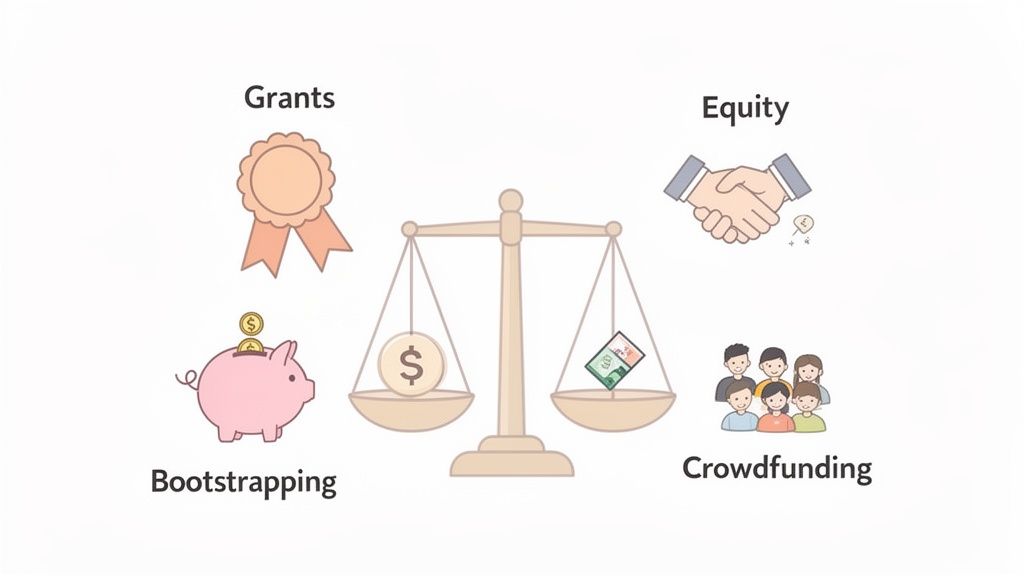

Exploring Funding Alternatives Beyond Debt

Taking on debt can feel like a rite of passage for many founders, but a startup company loan is far from your only path to growth. It’s easy to get tunnel vision and assume a loan is the default next step. That mindset, however, can close you off to other options that might be a much better fit for your company’s stage and your own tolerance for risk.

Every funding path comes with its own trade-offs between speed, cost, and control. Choosing the right one means getting honest about your vision. Do you want to maintain 100% ownership and answer to no one, or are you willing to trade a piece of the company for the capital and connections needed to scale fast?

The Path of Ultimate Control: Bootstrapping

Bootstrapping is the art of building your company from the ground up using nothing but your own revenue. It’s the ultimate path to discipline and control. Every dollar you earn is yours to reinvest, and you never have to justify your decisions to a board or a banker.

The upside is obvious: you keep full ownership and are forced to build a genuinely profitable business from day one. The catch? It’s slow. Your growth is tied directly to your cash flow, and you risk getting outpaced by a well-funded competitor.

Free Capital for Mission-Driven Work: Grants

Grants are essentially non-dilutive, non-repayable gifts. Think of it as "free" money awarded by governments, foundations, and corporations to businesses working on specific missions—like developing new tech, promoting sustainability, or solving a social problem.

Pros: You get capital you don’t have to pay back, and it doesn’t cost you any equity. Winning a prestigious grant also adds a huge amount of credibility to your startup.

Cons: The application process is often long, competitive, and bureaucratic. Grants are also highly specific, so your business must align perfectly with the grantor's goals.

Trading Equity for Capital and Connections

Equity financing is what most people picture when they hear "startup funding." This is the world of angel investors and venture capitalists (VCs), where you sell a percentage of your company in exchange for a check.

But this route is about more than just money. The right investors bring a network, deep industry expertise, and strategic guidance that can be invaluable. The flip side is you’re giving up a piece of your company and bringing on new stakeholders you'll have to answer to. This means more pressure to chase rapid growth and hit aggressive milestones.

For startups that can't offer physical collateral but still need significant capital without immediately giving up equity, other debt-based alternatives exist. For instance, the global market for unsecured business loans reached $253.9 billion in 2025. North America held the largest share, and small enterprises—like a typical SaaS team—accounted for 33.58% of this funding, often using it for tech upgrades. You can read more about the unsecured business loan market on straitsresearch.com.

The Power of the Crowd: Crowdfunding

Platforms like Kickstarter or Indiegogo let you raise small amounts of money from a huge number of people. It’s a fantastic way to validate a product idea, build an early community of passionate users, and generate buzz before you even launch.

The trade-off is that it requires a serious marketing effort to run a successful campaign. You need a compelling story and often a great demo video to capture attention and convince backers to support you. For founders looking to build momentum, it's worth exploring how to structure a narrative, and our guide on making effective training videos shares principles that apply here, too. A successful campaign isn't just about funding; it's about building a tribe.

Common Questions About Startup Company Loans

When you're trying to scale a company, the world of funding can feel intentionally confusing. You just want straight answers, not a three-hour lecture on financial derivatives. We've cut through the noise to answer the most pressing questions founders have about getting a startup loan.

How Soon Can a New Startup Get a Loan?

This is the classic chicken-and-egg problem for founders. It’s tough, but not impossible.

Most traditional banks want to see at least six to twelve months of consistent revenue before they’ll even talk to you. They’re in the business of minimizing risk, and a brand-new company is, by definition, a risk.

But the lending world has changed. Online lenders and fintech platforms specialize in newer businesses and often use different data to make decisions—like the strength of your personal credit, the clarity of your business plan, and early monthly recurring revenue (MRR).

If you're pre-revenue, don't count yourself out. SBA microloans are often more accessible to very early-stage startups than larger bank loans. The key is to find a lender whose risk profile aligns with your company's stage. You wouldn't pitch a seed-stage idea to a late-stage VC, and the same logic applies here.

Can I Get a Startup Loan with Bad Personal Credit?

This is a major hurdle. Lenders often see your personal credit history as a direct reflection of your financial reliability, and a low score makes them nervous. It’s definitely harder with bad credit, but you still have options.

Your best bet is to find lenders who put more weight on your business's performance than your personal score.

Focus on Revenue: Some lenders, particularly in the fintech space, will prioritize your business's cash flow. If you have strong, consistent sales, this can sometimes outweigh a weaker credit score.

Offer Collateral: If you have business assets like equipment or inventory, you can offer them as collateral for a secured loan. This reduces the lender's risk and can make them more willing to say yes.

Explore Alternatives: Options like revenue-based financing or invoice factoring are based on your sales, not your FICO score. If your sales are strong, these can be great paths to capital.

The bottom line is that working to improve your personal credit score before you apply will always open more doors and get you better interest rates. It's a foundational step that pays long-term dividends.

What Are the Most Common Reasons for Loan Rejection?

Getting a "no" is frustrating, but understanding why is the only way to succeed on your next try. Rejections rarely come out of nowhere; they usually point to a specific weakness in the application.

Here are the most common deal-breakers:

A Weak or Vague Business Plan: Lenders need to see a clear, logical path to repayment. If your plan is full of buzzwords but lacks concrete financial projections, it's a huge red flag.

Poor Credit History: Both personal and business credit scores get scrutinized. A history of late payments or defaults signals high risk.

Insufficient Cash Flow: Your business has to generate enough cash to cover its existing expenses plus the new loan payment. If your margins are too thin, you'll likely be denied.

High Debt-to-Income Ratio: If you or your business is already carrying a lot of debt, lenders will be hesitant to add more to the pile.

An Unfocused "Use of Funds" Request: Asking for money without a precise plan for how it will generate a return is a fast track to rejection. Lenders want to fund specific growth initiatives, not vague hopes.

Applying to the wrong type of lender for your startup's stage is another frequent, and entirely avoidable, mistake. Do your homework and target lenders who have a history of funding companies like yours.

Does a Startup Loan Affect My Personal Finances?

Yes, it almost always does. This is a critical point that many founders overlook in their rush to get capital.

The connection between your business debt and your personal finances is forged by a single, powerful legal document: the personal guarantee.

A personal guarantee is a clause where you promise to repay the debt yourself if the business can't. This means that if your company fails, the lender can legally come after your personal assets—your savings, your car, even your house. It’s their insurance policy.

Nearly every startup lender will require a personal guarantee from the founders. The application process itself also involves a hard credit check, which will temporarily ding your personal score by a few points. It’s absolutely vital to understand this deep connection before you sign anything.

Creating a clear, compelling story for your product is just as important as having your finances in order. A sharp product demo can make the difference between a confused lender and a confident partner. Forgeclips helps SaaS companies create studio-quality demo and promo videos fast, using a framework-based approach that prioritizes clarity and conversion over high-production fluff. If you need to show your product's value in under two minutes, check out our structured video frameworks.