Getting a loan for a startup company can feel like a classic catch-22. You need cash to prove your model, but lenders want to see a proven model before they give you any cash. It's a frustrating loop, but one you can absolutely break. The trick is to stop scrambling for capital and start with a strategic, honest look at your own readiness.

Where to Even Begin with a Startup Loan

Let's be real—the moment you realize you need outside funding is both thrilling and terrifying. Your idea is finally taking off, but your bank account can't keep up. The first hurdle isn’t just finding a lender; it's figuring out if you're even prepared to apply and where you should look. It feels overwhelming before you’ve filled out a single form.

I’ve been there. My early attempts at securing funding felt like shouting into the void. Traditional banks were slow, their processes were rigid, and they seemed allergic to any business that wasn't a brick-and-mortar store. Trying to explain a SaaS business felt like describing the cloud to someone who only understands inventory financing.

The Modern Lending Shift

Thankfully, the lending world has changed dramatically. The global fintech lending market soared to $590 billion in 2025, completely changing how startups get funded. Digital lending now drives 63% of all U.S. personal loan originations, and over half of small-business loans in developed countries come directly from fintech platforms. For founders who can't afford to get bogged down by old-school bureaucracy, this shift is everything.

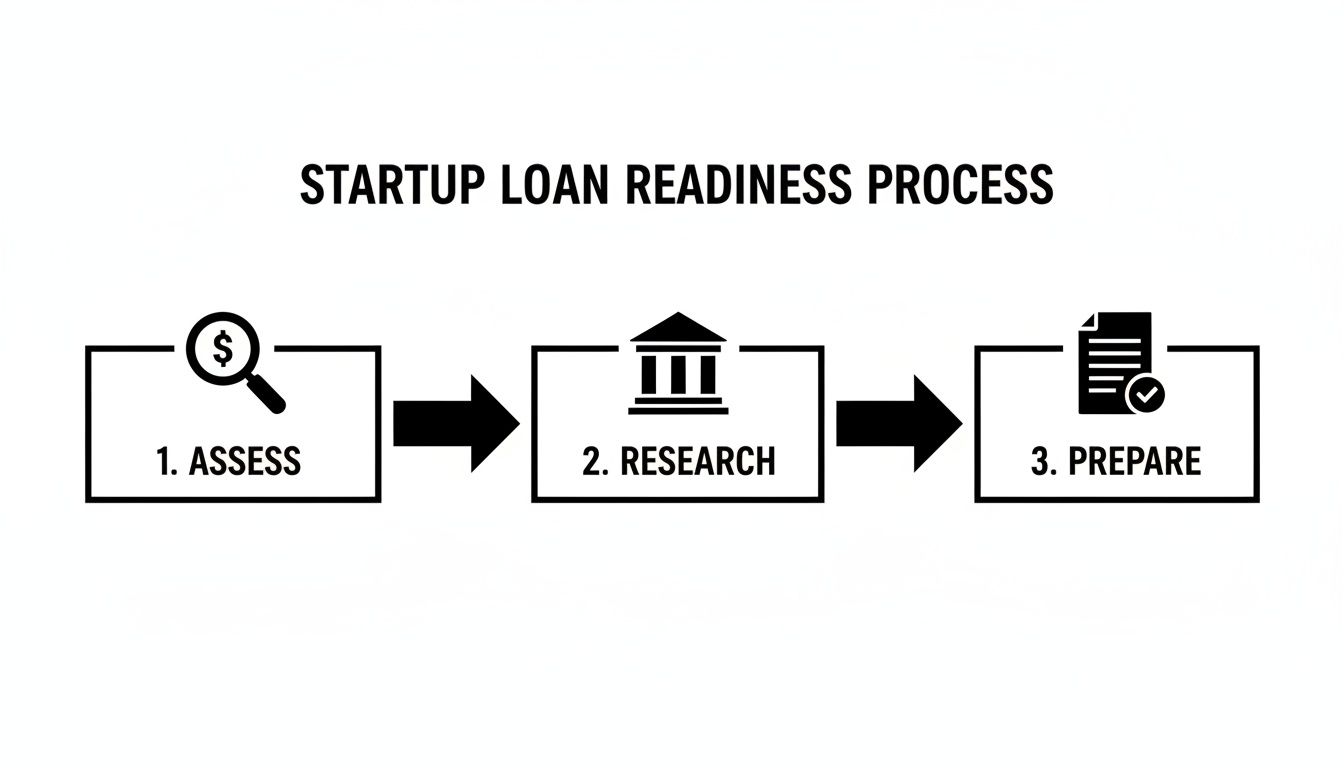

This process map breaks down the foundational steps to take long before you ever fill out an application.

Following this simple framework—assess, research, prepare—ensures you approach lenders from a position of strength, not desperation. Before you get lost in specific loan types, it's smart to understand the big picture, which includes getting familiar with some legal tips for raising capital.

The goal isn’t just to get a 'yes' from a lender. It's to get the right 'yes' on terms that won't cripple your business a year from now. A realistic self-assessment is your best defense against bad debt.

Performing a Realistic Self-Assessment

Before you even think about lenders, you need to look inward. A brutally honest self-assessment is the most critical first step. It forces you to get organized and gives you the clarity to build a case that’s impossible to ignore.

Start by asking yourself these core questions:

How much do I really need? Don’t just pull a number from thin air. Break it down into specific line items: server costs for six months, a small budget for initial marketing, or key software licenses. Get granular.

What is my personal financial situation? Lenders will absolutely scrutinize your personal credit score and any assets you hold. A score below 640 can be a major roadblock with traditional lenders.

Have I put my own money in? This is what lenders call having "skin in the game." They are far more willing to bet on you if you've already bet on yourself.

Can I clearly articulate my business? You need a simple, compelling story. What problem do you solve, who is your customer, and how will you make money? If you're just getting started, our guide on how to start a startup company can give you more foundational advice.

Answering these questions builds a strong foundation. It turns your loan request from a hopeful ask into a well-reasoned business proposal, giving you the confidence to navigate the next steps with a clear head.

Choosing the Right Loan for Your Startup

Getting a loan isn't the victory. Getting the right loan is. I've seen more than a few founders get locked into punishing terms that suffocated their startup before it ever had a chance to breathe. This isn't just about finding cash; it's about finding the right kind of capital for your specific needs.

The loan that's perfect for a local coffee shop buying an espresso machine is a total disaster for a SaaS company trying to scale its cloud infrastructure. You have to match the financing to the mission.

Let’s walk through the main options you’ll encounter.

SBA Loans: The Government-Backed Path

When you hear someone talk about a loan for a startup company, they're often thinking of SBA loans. But the Small Business Administration doesn't actually cut the checks. Instead, it guarantees a large portion of the loan for a partner bank, which makes lenders far more willing to take a risk on a new venture.

The SBA has become a serious engine for new businesses. In Fiscal Year 2025, it backed 84,400 loans totaling a massive $44.8 billion. And for founders, the important number is this: 8,900 of those loans, worth $5.6 billion, went straight to startups.

These aren't just for traditional businesses, either. SaaS founders and indie hackers are getting this funding, proving you don't always need to chase VC money.

Here are the two programs that matter most for startups:

SBA 7(a) Loans: This is the SBA’s flagship program because it’s so flexible. You can use the funds for working capital, hiring, marketing, or even buying commercial real estate. The catch? The application is demanding. You’ll need a rock-solid business plan, good personal credit, and almost certainly a personal guarantee.

SBA Microloans: As the name suggests, these are smaller loans, capped at $50,000. They come from nonprofit community lenders, not big banks. They're perfect for covering initial software licenses, a small marketing blitz, or getting your first office space. The requirements are generally less strict than for a 7(a) loan.

Traditional Term Loans and Lines of Credit

Outside of government programs, you have the classic financing options directly from banks and online lenders. These are often simpler products but can be a tougher sell for a company without a long history.

A term loan is straightforward: you get a lump sum of cash upfront and pay it back, with interest, over a fixed period. This is your go-to for a large, defined expense. I know a founder who used a small term loan to buy a block of dedicated servers—a clear, one-time purchase with a predictable return.

A business line of credit is entirely different. It acts like a credit card for your business. You’re approved for a certain limit and can draw cash as you need it, only paying interest on what you actually borrow.

This is the ultimate tool for managing choppy cash flow. A friend of mine who's an indie hacker uses his line of credit to cover server bills and ad spend between product launches. It gives him incredible flexibility while he waits for revenue to ramp up, without the weight of a big loan payment.

Niche Financing for Specific Needs

Sometimes a general-purpose loan just doesn't fit. A couple of specialized options are often overlooked but can be a game-changer for the right startup.

Equipment Financing

This is exactly what it sounds like: a loan to buy physical equipment. The major advantage is that the asset you’re buying acts as collateral, making it much easier to get approved.

And don't just think of heavy machinery. For tech startups, "equipment" can mean:

High-performance servers and networking hardware

A fleet of powerful laptops for your engineering team

Professional-grade video and podcasting gear

If you need to buy a tangible asset, this is one of the smartest ways to do it without burning through your operating cash.

Revenue-Based Financing (RBF)

For SaaS, e-commerce, and other startups with recurring revenue, RBF has become a powerful alternative to traditional debt. Instead of a loan, you get a cash advance. In return, you agree to pay the lender a small percentage of your future monthly revenue until the advance is paid back, plus a flat fee.

Your payments rise and fall with your sales, which removes the stress of a fixed monthly payment when you're in growth mode. The lender is betting on your success—they get paid back faster when you grow. It's a great way to get non-dilutive capital if you have predictable income. If you want to see how this model has worked for others, you can check out some great business loan case studies for startups.

Preparing Your Financials and Documents

Nothing kills a loan application faster than messy documents. Walking into a lender meeting—virtual or not—with a disorganized folder signals you aren't serious and, worse, that you don't have control over your business.

This isn't just about checking off boxes on a list. It’s about building a bulletproof loan package that anticipates every question a lender will throw at you. This preparation alone can be the difference between a quick "no" and a term sheet. Your goal is to project credibility, organization, and total command of your numbers.

More Than Just a Checklist

Your loan application tells a story, and that story needs to be backed by cold, hard data. Lenders aren't funding a big vision; they’re funding a well-researched plan. They are, first and foremost, risk managers.

Every document you provide must work together to build a compelling narrative of manageable risk and predictable repayment. It's your job to de-risk your startup in their eyes.

Key Insight: Lenders don’t fund dreams; they fund plans. They need to see a clear, data-driven path to getting their money back, with interest. Your entire package should be built around answering that one fundamental concern.

Crafting a Lender-Friendly Business Plan

A business plan for a lender is not the same as a pitch deck for a venture capitalist. A VC might get excited by a massive total addressable market, but a lender cares far more about your specific, achievable milestones over the next 12-24 months.

Your plan needs to clearly articulate:

The Problem and Your Solution: State it simply. Who is your customer, and what pain point are you solving? No jargon.

Market Analysis: Don't just say "the market is huge." Provide data on your specific niche. Who are your direct competitors, and what’s your real, sustainable advantage?

Marketing and Sales Strategy: "Running Facebook ads" isn't a strategy. A real strategy sounds like this: "We will allocate $5,000 to a targeted ad campaign aimed at project managers in the tech industry, with an expected CAC of $50 and a projected LTV of $450." Be specific.

Management Team: Highlight relevant experience. If you’re a solo founder, lean into your own domain expertise and the advisors you’ve assembled.

If you need to tighten up your core business concept, our guide on how to start a startup company offers foundational principles that will help you articulate this section with clarity.

Building Realistic Financial Projections

This is where the rubber meets the road—and where most applications fall apart. Your financial projections are the heart of your request. They must be ambitious enough to be interesting but grounded enough to be believable.

Lenders will scrutinize your Profit & Loss (P&L), Cash Flow Statement, and Balance Sheet. A comprehensive 3 statement financial model is almost always required, as it gives them a complete, interconnected view of your startup's financial health.

Make your numbers credible by doing the following:

Justify your revenue. Don’t just invent figures. Build your forecast from the bottom up. If your SaaS is $20/month, show the math: how many new customers can you realistically acquire each month based on your marketing spend and conversion rates?

Detail every expense. Be exhaustive. Include software subscriptions, server costs, salaries, marketing spend—everything. Slightly over-budgeting for expenses shows you’re prepared for the unexpected.

Show your assumptions. Have an "Assumptions" tab in your spreadsheet. This is where you explain why you believe your customer churn will be 5% or your ad conversion rate will be 2%. Link these assumptions to market data or early traction.

Stress-test your model. What happens if sales come in 50% lower than you projected? What if a key expense doubles? Showcasing that you’ve run a worst-case scenario demonstrates maturity and foresight. Lenders love this.

How to Craft a Pitch That Actually Resonates With Lenders

Your loan application is not a VC pitch. I see founders make this mistake constantly—they walk in armed with grand visions and hockey-stick growth charts, only to be met with blank stares and a swift rejection.

Here's the truth: lenders are financiers, not dreamers. They are fundamentally risk-averse, and their entire evaluation process boils down to one simple question: "How will I get my money back?"

Your entire pitch, from start to finish, must be a clear, logical, and structured answer to that single question.

Translate Your Vision Into Repayment Math

You have to learn to speak their language. That means translating your startup's potential into the cold, hard mechanics of debt service. Frame your value proposition, market opportunity, and growth strategy through the lens of repayment ability.

Forget the marketing jargon. Focus on demonstrating a clear and believable path to profitability that covers the loan payments with a healthy buffer. This means breaking down your story into the metrics they care about:

Customer Acquisition Cost (CAC): What does it cost to acquire a single paying customer?

Lifetime Value (LTV): How much revenue will that customer generate for you over time?

Time to Profitability: When will your revenue consistently exceed all expenses, including this new loan?

When you can show that a $50 CAC generates a $450 LTV, you're no longer selling a dream. You’re showing them that every dollar they lend you has a measurable, positive return that directly funds repayment.

A lender doesn't need to believe in your mission as much as they need to believe in your math. The best pitch makes the decision to lend feel like a logical, low-risk business transaction, not a leap of faith.

Your Secret Weapon: A Short, No-Frills Demo Video

Spreadsheets and business plans are abstract. This is especially true if you’re building a SaaS product or complex software. A short, clear product demo video makes your vision tangible and proves you've actually built something real.

This is not the time for a slick, expensive marketing video. In fact, it's the opposite. A simple, well-structured video that walks a lender through your product's core workflow is infinitely more powerful than a dozen pages of text. It shows, it doesn't just tell.

A strong demo video for a lender should follow a simple, direct path:

Expose the Problem: Visually show the specific pain point your product solves.

Introduce the Solution: Demonstrate the one core feature that delivers relief.

Show the Outcome: Display the clear, positive result for the user.

Using a framework for this ensures your video is direct and effective, answering a lender's unasked questions. You can build one quickly with a simple structure, and our explainer video script template is a great place to start. This approach replaces high-production fluff with the kind of grounded clarity that gives a risk-averse lender confidence. It shows them a real product, built by a serious founder.

Navigating the Application and Negotiation

You hit "submit." All the documents are in, the business plan is uploaded, and now... the waiting game begins. This part of the process can be even more nerve-wracking than the prep work, a real test of your patience and persistence.

But getting a loan for a startup company isn’t just about securing an approval. It's about getting terms that won't cripple your growth later on. Knowing how to handle what comes next is where the real work begins.

From Submission to Decision

Once your application is in, it goes into underwriting. A loan officer or credit analyst will comb through every document, verify your numbers, and run credit checks. The timeline here varies wildly. A modern fintech lender might have an answer for you in 24-48 hours, while an SBA loan can take anywhere from 30-90 days.

It’s perfectly fine to follow up, but you have to be strategic. A short, polite email a week or two after submitting to ask if they need anything else shows you’re engaged, not desperate. If they ask for more info, send it over immediately. Speed and professionalism at this stage reinforce that you're an organized and reliable partner.

A "no" isn't a dead end. If you get rejected, always ask for the specific reasons why. This feedback is gold. A common reason for denial, especially in the current climate, is existing debt. In fact, 41% of denied applicants in the U.S. cited 'too much debt' as the reason in 2024, a huge jump from just 22% in 2021.

This data, along with a massive $5.7 trillion finance gap for small and medium-sized businesses, shows just how competitive the lending environment is. Globally, 38% of employer firms sought financing in the past year, and while online fintech lenders are gaining ground, 60% of their borrowers complain about high costs. You can get a deeper look at the numbers in the full World Bank report on SME finance.

Dissecting the Loan Offer

When that term sheet finally lands in your inbox, the work isn't over. Don't let the excitement of an approval cause you to gloss over the details. The interest rate gets all the attention, but it’s the fine print that can make or break your company’s future.

Pay close attention to these key terms:

Interest Rate and APR: The interest rate is the basic cost of borrowing, but the Annual Percentage Rate (APR) is the real number. It includes all the fees and other charges, so always compare APRs for a true side-by-side analysis.

Loan Covenants: These are the rules of the road you have to follow to keep the loan in good standing. Covenants can be positive (like maintaining a certain debt-to-equity ratio) or negative (like being prohibited from taking on more debt without permission). Breaking them can trigger a default, so read them carefully.

Prepayment Penalties: Some loans will actually charge you a fee for paying them off early. This is a term you should almost always try to negotiate away, as it kills your financial flexibility if you have a sudden cash windfall.

The Personal Guarantee: We’ve hit this point before, but it’s critical. This clause makes you personally responsible for the debt if the business goes under. For most startup loans, this is non-negotiable, but you have to understand exactly what you're signing.

Negotiation isn’t just about demanding a lower rate. It’s about building a partnership that works for both you and the lender. Your strongest leverage comes from having a stellar financial profile or, even better, competing offers.

Before you even start the conversation, know what’s most critical for your startup. Is a longer repayment term more valuable than a slightly lower interest rate? Know your priorities, and you'll be negotiating from a position of strength.

Your Startup Loan Questions, Answered

The world of startup funding is filled with "what if" scenarios that can keep you up at night. Even the most buttoned-up plan has loose ends. Let’s cut through the noise and give you direct answers to the most common questions we hear from founders trying to land a loan for their startup company.

Can I Get a Startup Loan With No Revenue or Bad Credit?

Let's be blunt: this is the toughest hill to climb. But it's not always impossible. With zero revenue on the books, lenders have nothing to go on but your business plan, your personal credit score, and any collateral you can bring to the table.

A "bad" personal credit score—usually anything below 640—is a dealbreaker for most traditional banks. However, some online lenders and microfinance institutions play in this space. They might offer you a smaller loan, but expect significantly higher interest rates to cover their risk.

If you’re in this situation, your only shot rests on three things:

A Bulletproof Business Plan: Your market research and financial projections need to be airtight and incredibly compelling.

"Skin in the Game": You have to show you've already invested a serious amount of your own money.

A Co-signer: Getting a business partner or family member with strong credit to co-sign the loan can change the entire conversation.

Be prepared for intense scrutiny. Lenders need to be completely convinced your idea is powerful enough to overcome the massive red flag of having no financial track record.

What Are the Most Common Reasons a Startup Loan Is Denied?

Getting rejected stings, but it’s almost always for a specific, tangible reason. If you know why lenders say "no," you can avoid those mistakes from the get-go.

The usual suspects are a weak business plan, unrealistic financial forecasts, and a poor personal credit score. Another huge red flag is a lack of founder investment—if you haven't bet on yourself, a lender definitely won't. Lenders also get skittish when there's a clear mismatch between how much you're asking for and what you plan to do with it.

Asking for "$200,000 for marketing" is a fast-track to rejection. A strong application says, "I need $200,000 to acquire 1,000 new customers at a projected CAC of $200, which will generate $500,000 in new ARR within 18 months." One is a wish; the other is a concrete plan.

What Are the Best Alternatives if I Cannot Get a Loan?

If the debt route just isn't working out, don't panic. Plenty of massively successful companies were built without ever taking on a traditional loan. The trick is to shift your focus to other ways of funding the business.

Here are the top alternatives you should be looking at:

Grants: Search for grants from government programs (like the SBIR) or private foundations in your niche. It’s essentially free cash, but be ready for a long and competitive application process.

Revenue-Based Financing (RBF): A fantastic choice for SaaS or e-commerce startups with predictable revenue. An investor gives you cash upfront in exchange for a small percentage of your future monthly revenue until a pre-agreed amount is repaid.

Equity Financing: This means selling a piece of your company to angel investors or venture capitalists. You get capital and often valuable expertise, but you’re giving up ownership.

Crowdfunding: Platforms like Kickstarter (for products) or Wefunder (for equity) let you raise smaller amounts of money from a large group of people.

Bootstrapping: The ultimate form of having "skin in the game." This is where you fund the business entirely from your personal savings or by reinvesting every dollar of early customer revenue back into growth.

How Does a Personal Guarantee Work for a Business Loan?

A personal guarantee is a legally binding contract that says you'll repay a business loan with your own money and assets if the company can't. It completely removes the liability shield between your business and your personal life.

This means if your startup goes under and defaults on the loan, the lender can legally come after your personal assets—your home, car, and savings accounts—to get their money back. Lenders demand this to lower their risk, especially when lending to new businesses with few corporate assets.

Nearly every startup loan, particularly from traditional banks and the SBA, will require a personal guarantee from any founder who owns 20% or more of the company. It’s a non-negotiable term in most situations, so make absolutely sure you understand what you're signing.

Crafting a clear product demo is one of the best ways to de-risk your startup in a lender's eyes. Instead of getting stuck in the DIY trap or overpaying an agency, Forgeclips offers a framework-based approach to create studio-quality demo and explainer videos fast. We help you build a video that shows your product's value and makes your pitch tangible.