Every founder knows the feeling. You’ve got traction, the machine is starting to hum, but your growth is burning cash faster than revenue can fill the tank. Suddenly, you're walking a financial tightrope, balancing payroll and ad spend, all while trying not to lose momentum. Relying only on revenue can strangle your growth right when you’re poised to take off.

Startup company loans are a strategic way to fund growth—like hiring, marketing, or expansion—without diluting your ownership. They act as a financial bridge, providing the capital needed to scale while you maintain full control of your company's direction and equity.

Walking The Cash Flow Tightrope

Every founder knows this feeling. You’ve got traction. Customers are coming in. The machine is finally starting to hum. But there’s a catch: your growth is burning through cash faster than revenue can fill the tank. Suddenly, you're walking a financial tightrope, balancing payroll, ad spend, and server bills, all while trying not to lose momentum.

This is that terrifying, exhilarating phase where you’re too successful to stop but not yet profitable enough to stand on your own. It's the exact point where bootstrapping often hits a wall. Relying only on your own revenue can end up strangling your growth right when you’re poised to take off.

The Problem with Premature Funding

For many founders, the knee-jerk reaction is to start chasing venture capital. But going after equity funding too early can be a huge mistake. You risk diluting your ownership for a valuation that doesn’t even begin to capture your startup's real potential. It's a classic trap: giving away a huge slice of your company just to solve what might be a temporary cash flow crunch. That path usually leads to more pressure, less control, and a board you suddenly have to answer to.

So, what's the alternative?

Debt financing shouldn't be a last resort. It's a strategic tool—a bridge that closes critical growth gaps without forcing you to sell off pieces of your company before you're ready.

A Bridge to Sustainable Growth

This is exactly where startup company loans come in. A loan gives you the capital you need, but on your terms. It lets you invest in that key hire, double down on a marketing channel that’s clearly working, or just cover your expenses while your monthly recurring revenue catches up. For a closer look at the early challenges of getting a business off the ground, check out our guide on how to start a startup.

When you use debt strategically, you can:

Retain 100% Ownership: You keep every bit of the equity you’ve bled for.

Maintain Control: You’re still the one making all the calls, no outside investors required.

Fuel Predictable Growth: You can fund specific, ROI-driven projects with a clear plan for repayment.

Once you understand how to use debt financing the right way, you can turn what seems like a liability into one of your most powerful assets for smart, sustainable growth.

A Founder's Guide To Startup Loan Types

Diving into the world of startup loans feels a lot like learning a new language. Words like “factoring,” “venture debt,” and “term loan” get thrown around, but what do they actually mean for your business? Picking the wrong funding is like using a sledgehammer to hang a picture—it might work, but you’re going to make a mess.

Let's cut through the jargon. This is your practical translation guide. We'll break down the most common loan types with real-world analogies, not dry definitions, so you can match the right capital to your specific needs. Understanding these options is the first step toward making a smart, strategic financing decision.

Quick Guide To Common Startup Loan Types

Before we get into the details, here’s a quick overview of the most common loan types, what they’re best for, and what to watch out for.

Loan Type

Best For

Typical Amount

Key Consideration

SBA Loan

Major, one-time investments like real estate or acquisitions.

$50,000 – $5M

Government-backed but the application is notoriously slow and paperwork-heavy.

Term Loan

Predictable, planned expansions with a clear ROI.

$25,000 – $500,000+

Straightforward, fixed payments, but requires strong credit and financials.

Line of Credit

Managing cash flow gaps and unexpected expenses.

$10,000 – $250,000

Flexible access to cash, but rates are often variable and can be high.

Equipment Financing

Purchasing machinery, tech, or vehicles.

Varies (tied to asset cost)

The equipment itself is the collateral, often making it easier to qualify for.

Invoice Factoring

B2B startups with long invoice payment cycles.

Varies (based on invoice value)

Immediate cash for unpaid invoices, but you sacrifice a percentage of the value.

Venture Debt

VC-backed startups needing to extend their runway.

$100,000 – $10M+

Non-dilutive capital, but often includes warrants (future equity).

This table is just a starting point. Now, let’s explore what makes each of these funding tools unique and how they fit into a founder’s toolkit.

SBA Loans: The Government-Backed Safety Net

An SBA loan isn't a direct loan from the government. Instead, the U.S. Small Business Administration (SBA) guarantees a huge chunk of the loan for the bank. Think of the SBA as the ultimate co-signer for your business. Because the bank’s risk plummets, they're far more willing to offer favorable terms—like lower interest rates and longer repayment periods—to startups that might otherwise get a "no."

This makes them a fantastic option for major, one-time investments.

Best For: Securing a big lump sum for a significant purchase, like buying commercial real estate, acquiring another company, or funding a massive initial inventory order.

Key Consideration: The application process is notoriously slow and bureaucratic. You'll need a rock-solid business plan and a healthy dose of patience, as approval can easily take months.

Term Loans: The Straightforward Classic

A term loan is the most traditional form of business debt you’ll find. You get a lump sum of cash upfront and pay it back, plus interest, over a set period (the “term”) with regular, fixed payments. It’s predictable and simple to budget for, just like a standard car loan—you know exactly what you owe each month and when you'll be done.

This structure makes it perfect for planned expansions or large projects where you have a clear, foreseeable return on investment.

A term loan provides a predictable financial runway for a specific, project-based goal. You can calculate the cost upfront and build it directly into your financial projections, removing the guesswork from your growth funding.

For example, a SaaS company might use a $100,000 term loan to fund a six-month marketing blitz with a proven customer acquisition cost (CAC), confident that the new monthly recurring revenue (MRR) will more than cover the payments.

Lines of Credit: Your Financial Buffer

A business line of credit works just like a credit card for your company. Instead of getting a lump sum, you’re approved for a preset amount of capital that you can draw from whenever you need it. You only pay interest on the money you actually use, and as you pay it back, the credit becomes available again.

This is your financial safety net, plain and simple. It’s perfect for navigating the unpredictable cash flow rollercoaster that every startup rides.

Best For: Covering unexpected expenses, bridging payroll during a slow sales month, or jumping on a sudden growth opportunity without needing to apply for a whole new loan.

Key Consideration: Interest rates are often variable and can be higher than term loans. Using a line of credit requires discipline—it should be a tool for emergencies, not a crutch for a broken business model.

Equipment Financing: Funding Your Tools

Does your startup depend on specific physical assets to operate? Equipment financing is designed for exactly that. The loan is used to buy machinery, vehicles, or technology, and the equipment itself serves as the collateral.

It’s a smart way to get the tools you need without draining your working capital. The lender’s risk is lower because they can repossess the asset if you default, which often leads to better rates and an easier qualification process.

Invoice Factoring: Unlocking Your Receivables

For B2B startups, waiting 30, 60, or even 90 days for clients to pay invoices can be a cash flow killer. Invoice factoring is the solution. A factoring company buys your outstanding invoices at a discount—usually paying you 80-90% of their value upfront—and then takes over collecting the payment from your client.

Think of it as selling your accounts receivable for immediate cash. Once your client pays the factoring company, you get the remaining balance, minus the factor’s fee. It’s a powerful tool for businesses stuck with long payment cycles.

This visual nails the tightrope act founders perform, where external financing like invoice factoring can inject immediate cash without forcing them to give up precious equity.

Venture Debt: The Pre-VC Growth Fuel

Venture debt is a special type of loan for startups that have already raised equity from venture capitalists. It’s typically offered alongside or between equity rounds (like a Series A or B). Lenders offer this capital because having VCs on board is a massive vote of confidence in the company's potential.

Founders often use it to extend their runway, buying more time to hit key milestones before raising a larger equity round at a much higher valuation. The trade-off? In exchange for the risk, venture debt lenders usually receive warrants, which are options to buy a small amount of equity in the future.

These alternative financing options are also getting a massive boost from the fintech world. The fintech lending sector recently saw a huge surge, with private company financing hitting nearly $14 billion in the first quarter alone—a 50% jump year-over-year. This explosive growth shows that non-traditional funding sources are no longer a niche play; they’re a mature and powerful part of the market. You can dig into more of these trends in these startup funding statistics.

How Lenders Evaluate Your Startup's Health

Applying for a startup loan can feel like sending your business plan into a black box. You hand over your financials, cross your fingers, and hope for the best. But what happens on the other side isn't magic—it's a methodical risk assessment.

Lenders are really just trying to answer one question: "If we give you this money, how sure are we that you'll pay it back?"

For a SaaS or tech startup, this gets complicated. Unlike a coffee shop with a lease and expensive espresso machines, your most valuable assets are often intangible. We’re talking about code, intellectual property, and monthly recurring revenue. This forces lenders to look beyond the old-school metrics and see your business through a more modern lens.

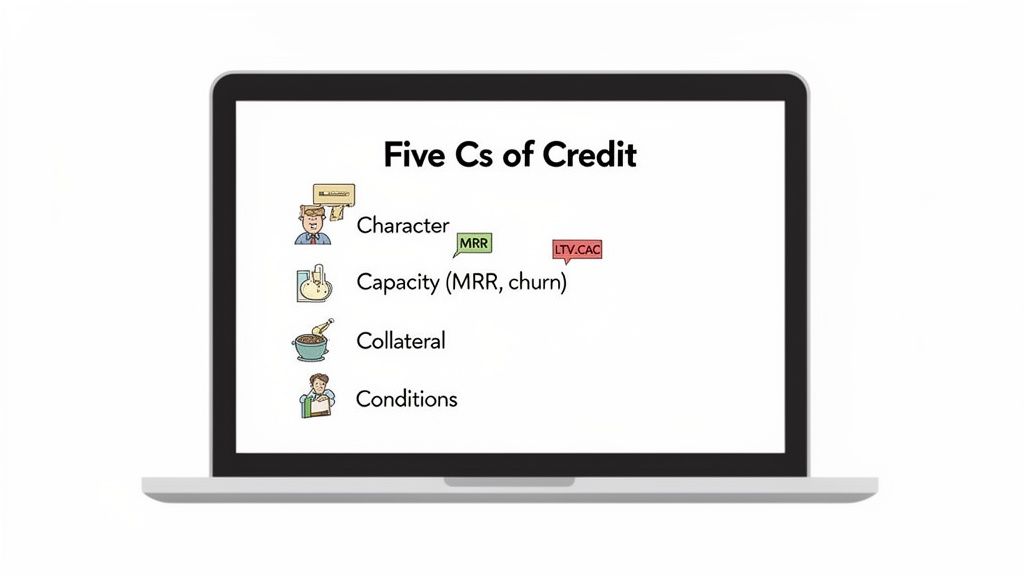

Translating the Five Cs of Credit for Startups

For decades, banks have leaned on a framework called the Five Cs of Credit. But for a business built on subscriptions and software, those terms need a bit of a translation.

Character: This is all about your track record and credibility. Lenders will pull your personal credit score (they're typically looking for 670 or higher) and any credit history your business has. They're also sizing up the founders. Do you actually have the industry experience to pull this off?

Capacity: In simple terms, can your cash flow cover the loan payments? For a SaaS startup, this has little to do with past annual profits. Instead, lenders will zoom in on your Monthly Recurring Revenue (MRR), churn rate, and cash flow statements. They need to see a steady, predictable income stream.

Capital: How much of your own money is in the business? This shows lenders you have real skin in the game. When you’ve put your own funds on the line, you’re far more motivated to see the company succeed, which naturally lowers their risk.

Collateral: This is an asset you pledge to secure the loan in case things go south. SaaS companies don't have warehouses full of inventory, so lenders might look at your accounts receivable or, more commonly, require a personal guarantee. This makes you personally responsible for the debt if the business can't pay.

Conditions: This covers the "why" behind the loan. Lenders need to see a clear, logical plan for the money. Are you hiring two desperately needed engineers to build out a feature customers are already begging for? Or are you just trying to float payroll for a few more months? The story matters.

Your Pre-Application Document Checklist

Showing up to a loan application unprepared is the fastest way to get a "no." Getting your documents in order first proves you’re serious and makes the underwriter’s job much easier.

Think of your application package as the business case for your loan. It should tell a clear and compelling story of where your company is, where it's going, and why this capital is the key to getting there.

While every lender is a bit different, gathering these documents ahead of time will dramatically speed things up.

Financial Documents

Business Financial Statements: This means your balance sheet, income statement (P&L), and cash flow statement for the last two or three years, if you've been around that long.

Business Bank Statements: Be ready to provide the last six to twelve months of statements so they can verify your revenue and cash flow firsthand.

Financial Projections: You'll need detailed, month-by-month projections for at least the next 12 months—often for the next three years. And you absolutely must be able to defend your assumptions.

Business and Personal Information

Detailed Business Plan: This needs to cover your business model, market analysis, team, and growth strategy. It has to clearly show how you'll use the loan to get results.

Personal Financial Statements: Lenders want to see your personal balance sheet, especially if a personal guarantee is on the table.

Business and Personal Tax Returns: The last two years of returns are pretty standard.

Legal Documents: Have your articles of incorporation, business licenses, and any major client or vendor contracts ready to go.

Pulling all this together is a heavy lift, but it's completely non-negotiable. For a deeper look at what to expect, we have other resources that break down the process of applying for a business loan for a startup company. Being organized doesn’t just make you a more attractive borrower; it forces you to take a hard, honest look at your own business before a lender does.

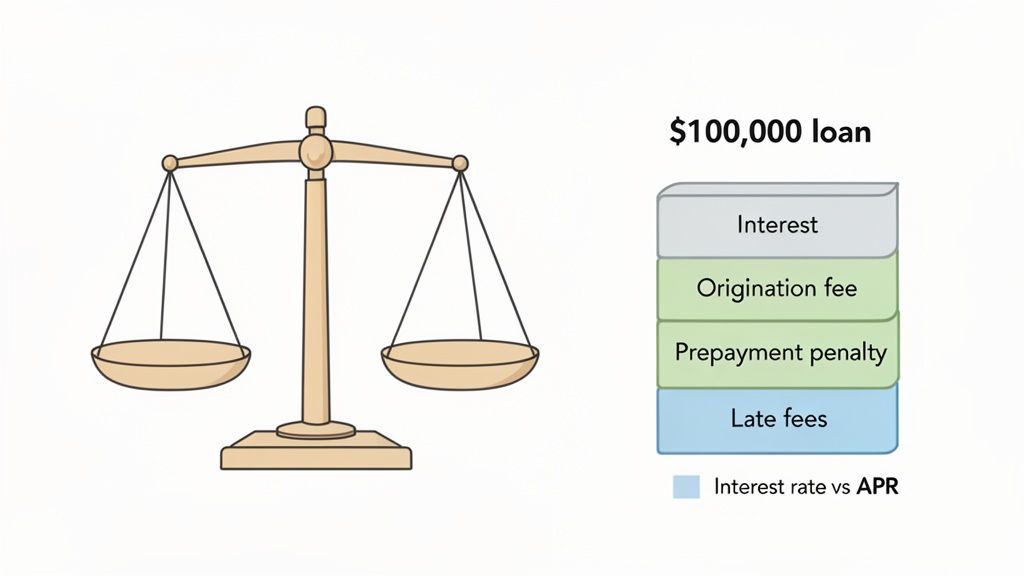

Understanding The True Cost Of Your Loan

Loan offers can feel like comparing apples and oranges. One lender might dangle a low interest rate, while another boasts about having "no hidden fees" but starts with a higher rate. The sticker price—that interest rate—is just the opening act. The real cost of a startup loan is a mix of that rate plus a handful of fees that can quietly inflate what you actually repay.

To make a smart decision, you have to look past the headline number and calculate the total cost of borrowing. It’s the only way to compare different offers on a level playing field and avoid a deal that looks cheap upfront but costs you way more in the long run.

Why APR Is Your Most Honest Metric

The single most important number to get your head around is the Annual Percentage Rate (APR). While the interest rate just covers the cost of borrowing the money, the APR gives you the full, unvarnished picture.

APR includes the interest rate plus most of the lender's fees, all rolled into a single yearly percentage. It's the closest you can get to an all-in cost of capital, making it the best tool for an apples-to-apples comparison between loan options.

A loan with a 7% interest rate but a high origination fee could easily have a higher APR than a loan with an 8.5% interest rate and zero fees. Always, always ask for the APR. If a lender is hesitant to give it to you, that’s a massive red flag.

Uncovering The Hidden Costs

Beyond the interest rate, a few common fees can dramatically change the total cost of your loan. You need to read the fine print and account for every single one.

Origination Fees: This is a one-time fee the lender charges just for processing and funding your loan. It's usually a percentage of the total loan, often between 1% and 6%, and it’s typically deducted from the funds you receive. So, on a $100,000 loan with a 3% origination fee, you’d only get $97,000 in your bank account but would be on the hook for repaying the full $100,000.

Prepayment Penalties: Believe it or not, some lenders charge you a fee if you pay off your loan early. It sounds completely backward, but they do this to guarantee they make a certain amount of profit from interest payments over the life of the loan. Always check for this clause if you think you might be able to clear the debt ahead of schedule.

Late Payment Charges: This one’s more straightforward. Miss a payment deadline, and you’ll almost always get hit with a penalty, which could be a flat fee or a percentage of what you owe.

Getting funding is competitive, and lenders are tightening their standards. Recent data shows that of the 59% of employer firms that applied for new capital, a stunning 24% received no financing at all. A key reason for denial was having too much existing debt, a factor cited by 41% of rejected applicants.

This just highlights why understanding the full cost of a new loan is so critical to your startup’s financial health. You can dig into the full report on these small business credit trends to see what lenders are looking for.

When To Choose Debt Over Equity

The debt versus equity debate isn't about which one is inherently "better." The real question is, which tool is right for the specific job you need to get done, right now?

Choosing between a startup company loan and selling off a piece of your company is one of the heaviest decisions a founder will ever make. It shapes everything—your cash flow, your control, your cap table, and your long-term relationship with the business you're building.

Keeping Control of Your Vision

Let’s be blunt: the biggest advantage of debt financing is simple but incredibly powerful. You keep 100% of your ownership.

When you take out a loan, you have a lender, not a new business partner. Lenders don't get a seat at your board meetings. They don’t have a say in your product roadmap, and they won't pressure you to pivot into a market you don't believe in.

Your obligation is purely financial. As long as you make your payments on time, you are free to run your company exactly how you see fit. That kind of autonomy is priceless, especially in the early days when your vision is still fragile and taking shape.

For founders who want to build a sustainable, long-term business on their own terms, debt provides the fuel for growth without forcing them to give up the steering wheel.

When you're thinking through funding strategies, it’s essential to understand the concept of non-dilutive funding. It's a category of capital that helps you grow without selling off shares, and business loans are a textbook example.

Debt Financing Vs Equity Financing At A Glance

To put this choice in the clearest possible terms, let’s break down how these two funding paths really differ on the factors that matter most to founders.

Factor

Startup Company Loans (Debt)

Venture Capital (Equity)

Ownership

You keep 100% of your equity.

You sell a percentage of your company.

Control

You retain full operational control.

Investors often gain board seats and influence.

Obligation

Repay a fixed amount on a set schedule.

Investors expect a massive (10x+) return.

Upside

You keep all future profits.

You share all future profits with investors.

Cost of Capital

Finite and predictable (interest and fees).

Potentially infinite (a % of future value).

This table doesn't tell you what to do, but it makes the trade-offs crystal clear. One path gives you total control with a predictable cost; the other gives you a partner and a shot at explosive growth, but at the cost of ownership.

Knowing When a Loan Makes Strategic Sense

Now, debt isn’t the right call for every single situation. It works best when you have a clear, predictable path to paying it back.

Here are a few scenarios where choosing a loan is the smarter play:

Funding Predictable Growth: You’ve found a marketing channel with a killer ROI or you need to hire one more engineer to finish a feature with proven demand. A loan lets you fund this specific, measurable growth without diluting your stake.

Bridging a Cash Flow Gap: You have signed contracts and revenue is definitely on its way, but there’s a 60-day lag in payments. A line of credit or invoice factoring can smooth things out without a permanent equity commitment.

Avoiding a Down Round: Maybe the market is shaky and valuations are low. Raising equity right now could mean a "down round," which is terrible for morale and momentum. Venture debt can extend your runway so you can raise capital later from a position of strength.

Tax Advantages: This is a nice little bonus. Unlike dividends you might pay to shareholders, the interest you pay on a business loan is typically tax-deductible, which can lower your overall tax bill.

Choosing a loan isn't a sign of desperation—it's a calculated business move. When used correctly, it’s a powerful, structured way to fuel performance-driven growth. Learning how to start a business is as much about mastering the strategic use of capital as it is about building a great product.

Exploring Alternative Funding Beyond Loans

While startup company loans are a fantastic tool, they aren't the only option on the menu. A truly resilient funding strategy is rarely built on a single source of capital. The smartest founders learn how to layer different types of financing to fuel growth at each stage—a practice known as 'capital stacking'.

Thinking beyond the bank opens up a world of possibilities that might be a better fit for your specific business model, especially if you're in SaaS. These alternatives can either complement a loan or replace it entirely, giving you far more flexibility and control.

Funding That Grows With You

For SaaS companies with predictable income, one of the most powerful alternatives is Revenue-Based Financing (RBF). Instead of a loan with fixed monthly payments, RBF providers give you a lump sum of cash in exchange for a small percentage of your future monthly revenue.

This model has two huge advantages:

Flexibility: Your payments are tied directly to performance. Have a slow month? You pay less. When sales spike, you pay a bit more. This natural alignment with your cash flow removes the pressure of a fixed payment schedule.

Speed: RBF applications are almost entirely data-driven, focusing on your MRR and growth metrics. This makes the whole process much faster than a traditional loan application.

Beyond Debt and Equity

Not all funding requires repayment or giving up a piece of your company. Every founder should keep these non-dilutive options on their radar.

Grants: This is essentially free money, often provided by government bodies, non-profits, or corporations to support innovation in specific fields. Grants are highly competitive but offer capital with zero strings attached.

Crowdfunding: Platforms like Kickstarter or Indiegogo let you pre-sell your product or raise funds from a large community of backers. This not only provides capital but also validates market demand before you even launch.

Angel Investors: While this is a form of equity, seeking small, strategic investments from angel investors can be a smart move. As you decide between debt or equity, understanding how to search for investors can clarify your path and connect you with individuals who offer mentorship alongside their capital.

Recent funding patterns reveal a powerful trend: companies that diversify their funding sources significantly outperform those that don't. While 73% of early-stage companies raised under $5 million, startups using four or more funding sources were 40% more likely to secure rounds over that amount. You can see more on how a diversified funding strategy accelerates growth in this startup economics report.

Ultimately, the goal is to build a financial foundation that is as innovative as your product itself. By combining loans with alternatives like RBF and grants, you create a more adaptable and resilient capital strategy. To explore the initial steps of this journey, you might be interested in our guide on how to start a startup company.

Your Startup Loan Questions, Answered

Founders always have the same core questions when it comes to borrowing money. Let's get right to them with some straight, no-fluff answers.

How much can a startup borrow?

This number is all over the map, and it really hinges on your business's health and which loan you're after. A brand-new startup might only get approved for a $10,000 line of credit to start. But a company with predictable monthly recurring revenue could easily secure a $500,000 term loan or even a multi-million dollar venture debt deal. Lenders are looking at your revenue, cash flow, personal credit, and the overall stability of your business. The more proven and predictable your income is, the more a lender is willing to put on the table.

What credit score is needed for a startup loan?

For most lenders, the magic number for a founder's personal credit score is at least 670. When your business is too young to have its own deep credit history, your personal score becomes the next best thing—a proxy for your financial reliability. A strong personal credit score tells a lender you have a track record of responsibly managing debt. For an early-stage company without years of financial data, this personal credibility can make or break an application.

Can I get a loan with no revenue?

It’s tough, but not entirely impossible. Getting a loan before you have any sales will seriously limit your options, and lenders will lean heavily on other factors. They'll put your business plan under a microscope, dig into your personal financial strength (like assets and that all-important credit score), and ask what collateral you can bring to the table. A few niche programs, like certain SBA microloans, are built specifically for pre-revenue businesses. For most traditional loans, however, showing some kind of consistent income is pretty much non-negotiable.

Is startup loan interest tax-deductible?

Yes. In most situations, the interest you pay on a business loan is considered a business expense and is tax-deductible. This is a huge deal, as it effectively lowers the true cost of your loan by reducing your company's taxable income. It’s one of the key financial advantages of using debt to grow. But tax rules are notoriously tricky, so always run this by a tax professional to make sure you're documenting and deducting everything by the book.

At Forgeclips, we turn complex product features into clear, high-performing videos that help you communicate value and drive growth. If you're building a great product, we can help you show it off. See how we do it at https://forgeclips.com.